Peaks2Tails

HOME

Product

All

Analytics

Stats for Finance

Risk and AI by GARP

Financial Modelling

New AGE Excel

Risk

PYTHON FOR RISK

Market and CPD Risk

Credit Risk Modelling

Deep Quant Finance

ICAAP, ILAAP and IRRBB

Sustainability Climate Risk

Trading

Cash Intraday

Bonds Techno Funda

DForum

Webinar

Resources

Login

Register

Home

Product

All

Analytics

Stats for Finance

Risk and AI by GARP

Financial Modelling

New AGE Excel

Risk

PYTHON FOR RISK

Market and CPD Risk

Credit Risk Modelling

Deep Quant Finance

ICAAP, ILAAP and IRRBB

Sustainability Climate Risk

Trading

Cash Intraday

Bonds Techno Funda

Dforum

Webinar

Resources

Register

Login

BOOTCAMP

Credit Risk Modeling

At a Glance

At a Glance

New AGE Excel

PYTHON FOR RISK

Stats for Finance

Risk and AI by GARP

Market and CPD Risk

Credit Risk Modelling

Cash Intraday

Deep Quant Finance

ICAAP, ILAAP and IRRBB

Bonds Techno Funda

Sustainability Climate Risk

BROCHURE

HANDBOOK

REGISTER

REGISTER

OVERVIEW

CURRICULUM

TRAINER

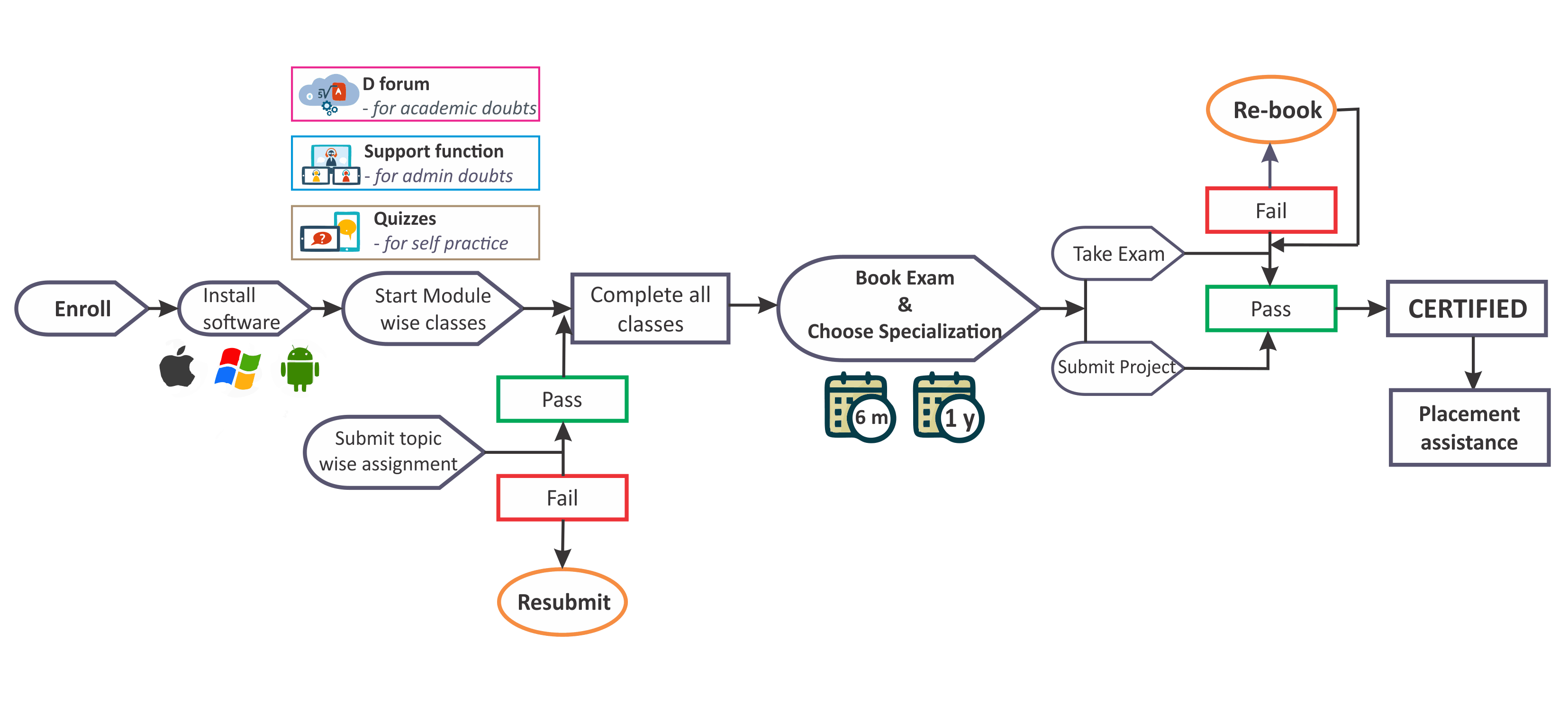

MODUS OPERANDI

FAQS

ABOUT THE TRAINER

1

OVERVIEW

2

CURRICULUM

3

TRAINER

4

MODUS OPERANDI

5

FAQ